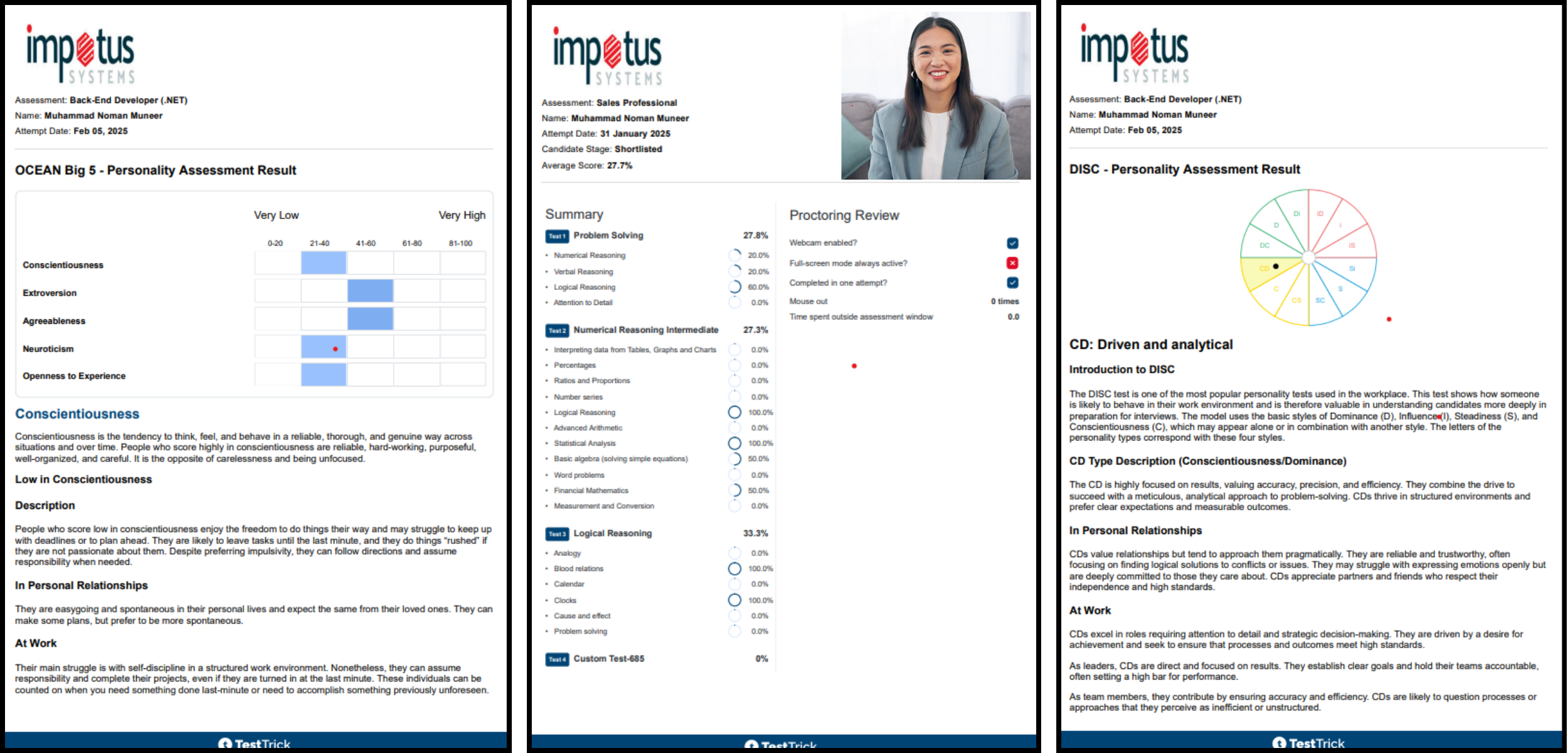

English

International Accounting Standard (Advanced) Test

The International Accounting Standard (Advanced) test is designed to evaluate in-depth knowledge and application of key International Accounting Standards (IAS), focusing on complex scenarios in financial statement presentation, asset management, and revenue recognition. This test ensures that candidates possess the advanced expertise required for compliance with global accounting standards.

Duration (Customizable)

16 min

Skills Covered

8

⭐Trusted by 1,000+ professionals worldwide

About the International Accounting Standard (Advanced) Test

The test then delves into IAS 16: Property, Plant, and Equipment, assessing candidates' skills in recognizing, revaluing, and depreciating tangible assets, as well as managing impairment and asset retirement obligations. It also includes IAS 18: Revenue (superseded by IFRS 15), where candidates must demonstrate an understanding of the transition to IFRS 15 and the complexities of revenue recognition in multi-element arrangements and long-term contracts. Furthermore, IAS 36: Impairment of Assets is examined, focusing on impairment testing methods and their impact on financial statements.

Finally, the test explores IAS 37: Provisions, Contingent Liabilities, and Contingent Assets, requiring candidates to apply judgment in recognizing and measuring provisions, and disclosing contingent liabilities and assets. It also covers IAS 38: Intangible Assets, assessing expertise in recognizing, amortizing, and impairing intangible assets, including internally generated ones. This rigorous assessment ensures that candidates are equipped to manage and report complex accounting issues in compliance with International Accounting Standards, enhancing the reliability and credibility of financial statements.

Covered Skills

IAS 1: Presentation of Financial Statements

IAS 2: Inventories

IAS 7: Statement of Cash Flows

IAS 16: Property, Plant, and Equipment

IAS 18: Revenue (superseded by IFRS 15)

IAS 36: Impairment of Assets

IAS 37: Provisions, Contingent Liabilities, and Contingent Assets

IAS 38: Intangible Assets

Test Details

Type

Role specific skills

Languages

English

Duration

16 minutes

Difficulty

Advanced

Recommended Job Roles to Use the International Accounting Standard (Advanced)

This test is ideal for seasoned accounting professionals, such as senior accountants, financial controllers, and auditors, who are responsible for preparing and auditing financial statements in accordance with International Accounting Standards. It is particularly relevant for those working in multinational corporations or firms where adherence to global accounting practices is essential for accurate financial reporting and decision-making.

Enhance Decision-Making with TestTrick's International Accounting Standard (Advanced) Detailed and Advanced Reports

Enhance your recruitment process with the most comprehensive International Accounting Standard (Advanced) and gain access to detailed and advanced reports. Utilize the Test to efficiently hire the perfect candidates 20x faster. Simplify your hiring process with our accessible solutions!

Transform Your Hiring Process with International Accounting Standard (Advanced) Test

Built-in & Customizable Assessments for Every Role

400+ Pre-Built Tests – covering cognitive, coding, and role-based assessments.

Create Custom Tests – tailor questions and formats to match your exact hiring needs.

Scientifically Validated Content – every built-in test is reviewed by subject matter experts for accuracy and fairness.

Flexible Question Types – from multiple choice to coding simulations, design assessments your way.

.png&w=3840&q=75)

Brand Your Assessments, Your Way

White-Label Experience – remove TestTrick branding and showcase your logo, colors, and tone.

Branded Communication – personalize email invites, landing pages, and candidate follow-ups.

Employer Branding Advantage – strengthen candidate trust and present your company as an employer of choice.

Professional Presentation – turn every assessment into a powerful reflection of your brand.

.png&w=3840&q=75)

Automated Scoring & Smart Candidate Management

Bulk Invitations & Smart Scheduling – invite hundreds of candidates in one go and set automated reminders.

Automatic Scoring – get instant results the moment candidates complete a test.

AI-Powered Insights – receive recommendations for top performers and borderline candidates.

Real-Time Reporting Dashboard – track progress, completion rates, and detailed results in one place.

AI-Powered Proctoring for Fair & Secure Assessments

Smart Candidate Monitoring – AI-based face detection, absentee tracking, and dual-screen detection.

Activity Tracking – screen & webcam recording, plus tab-switch monitoring to flag suspicious behavior.

Code Safety Controls – copy-paste disabling and detection of pasted code to ensure original work.

Real-Time Alerts & Reports – suspicious actions are flagged instantly, giving you confidence in results.

A Step-by-Step Process With Our Talent Assessment Software

Understand how TestTrick fits into your hiring process, from assigning tests to reviewing results and making decisions.

Set Up

Pick from our test library or build custom assessments for any job role.

Invite Candidates

Send assessments directly through your ATS or any other platform in a few clicks.

Track Performance

Use score cards or reports to review scores, code playback, and behavior logs.

Make Decisions

Collaborate with your team to compare results, spot skills gaps, and select candidates with confidence.

Advanced Proctoring Features

Comprehensive AI-powered monitoring and security features to maintain test integrity

AI-based Face Detection

Advanced AI detects and verifies candidate's face throughout the test, flagging multiple faces or absence to prevent impersonation.

Dual Screen Detection

Monitors and alerts when candidates use multiple screens or external monitors, marking violations for review.

Code Paste Detection

Tracks when candidates paste pre-written code instead of typing their own and flags the behavior for review.

Screen Recording

Captures screen activity and screenshots at intervals, allowing proctors to review unauthorized software use or suspicious behavior.

Webcam Monitoring

Takes camera shots at intervals to ensure continuous monitoring of identity and environment, preventing external help.

Tab Proctoring

Detects and flags when candidates switch between tabs or browsers to prevent searching for answers online.

Flag Suspicious Candidates

Automatically identifies candidates exhibiting unusual behavior like extended absences, dual monitors, or copy-paste attempts.

Copy-Paste Disabling

Disables copy-paste function during assessments to ensure originality and fairness in candidate responses.

Absentee Monitoring

Tracks assessment attempts and duration to help identify delays, missed attempts, and monitor participation.

Looking for Other Hiring Solutions?

Programming Tests

Evaluate coding proficiency across 50+ languages and frameworks with real-world coding challenges and algorithmic problems.

Role specific tests

Customized assessments for specific job roles including marketing, sales, finance, and management positions.

Psychometric tests

Measure personality traits, work preferences, and behavioral competencies to ensure cultural fit and team compatibility.

Cognitive ability tests

Assess problem-solving skills, logical reasoning, and analytical thinking capabilities for complex decision-making roles.

Frequently Asked Questions

Contact Us

FlyPearls LLC. 8 The Green # 4367 Dover, DE 19901 United States

+1 302 261 5361